Dear Shareholders and Friends of First Business Bank,

Our outstanding 2025 performance reflects our team’s exceptional execution of First Business

Bank’s long-term strategic plan. We expanded our client relationships, generating deposit and loan

growth that outpaced the industry. We continued our track record of double-digit annual growth, delivering

10% growth in top-line revenue and more than 14% growth in both pre-tax, pre-provision earnings1 and

earnings

per share. We continued to stack strategic successes into consistent and robust bottom-line results.

As I approach my retirement from First Business Bank this coming May, I am struck by how much has changed at

our company—and how much has remained steadfastly the same. This year’s annual letter offers a

special opportunity to not only discuss our most recent year of performance, but to also step back and

consider the longer arc of this organization: where we began, how we have evolved, and why we believe we are

exceptionally well positioned for the future.

A Strategic Plan Built for Consistency

One of the defining characteristics of First Business Bank has always been our commitment to long-term

strategic planning and – just as importantly – disciplined execution.

Our strategic plan is not a document we revisit once a year or set aside when conditions become challenging.

It is the framework that informs our decisions every day. We invest significant time and energy developing a

plan we believe in, and we measure ourselves against it consistently.

In 2025, that discipline mattered. Interest rate cuts, geopolitical events, and heightened competition all

factored in making it an unpredictable operating environment for banks. Against that backdrop, we did what

we’ve always done: control the controllable. We delivered another year of steady, dependable

performance. We met or exceeded all the long-term targets outlined in our 2024-2028 plan, reflecting the

strength of a diversified model working as intended.

Deposit growth remained central to our strategy. As a business-only bank, we have never operated a branch

network. This model suits our high-touch approach perfectly; however, it naturally limits deposit gathering

opportunities. From our earliest days, we understood that solving the deposit challenge would be critical to

building a sustainable business banking model. To that end, we’ve honed a deposit-centric sales

strategy led by treasury management sales teams located across our bank markets. Our bankers are trained and

incentivized to fund their loan production goals with deposit growth goals. Without the expense of operating

a branch network, we can offer very competitive rates that drive client loyalty while still achieving our

profitability goals.

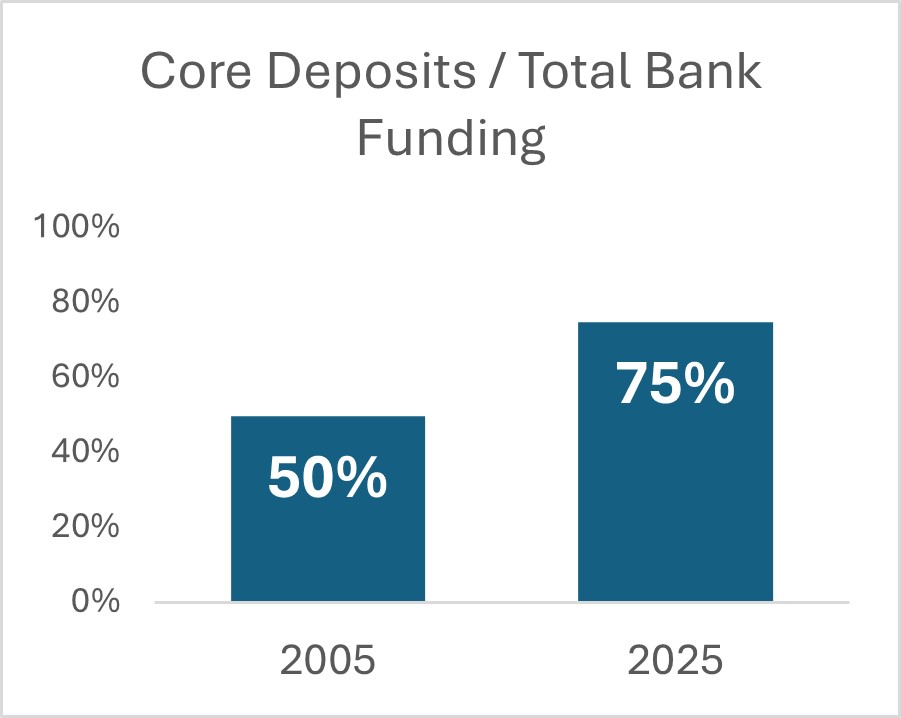

Our deposit focus has never wavered, and in 2025 it once again proved to be a differentiator. We grew

core deposits 12% over 2024, improving our core deposit funding mix to 75% at year-end. This reflects

significant growth compared to our 50% mix when we went public 20 years ago. Continued growth in

relationships drove this improvement. We track the treasury management fees we earn from providing

deposit services as a proxy for relationship growth, and this metric grew at an average annual rate of

over 11% over the past five years.

At the same time, we continued to benefit from a more diversified revenue base than at any point in our

history. Net interest income and fee income both contributed meaningfully to 2025 results, supported by

private wealth management, treasury management, specialty finance, and other fee-generating businesses

that did not exist when the bank was founded.

Consistency is not accidental. It is the product of planning, diversification, and execution—and it

is what allows us to look ahead with confidence.

An Organization That Has Evolved—By Design

To appreciate where we are today, it is worth briefly revisiting where we began.

Jerry Smith founded the bank in 1990 around a then-unconventional idea: an innovative business bank without

branches, focused on relationships, disciplined credit, and a matched-funding strategy. Some tactics have

evolved— remote deposit capture replaced a courier service that picked up clients’ deposits, for

example — but the core principles have endured.

In the mid-1990s, our business was concentrated in a single market, with a limited set of deposit, lending,

and fee-based offerings. We offered C&I and CRE loans alongside treasury management solutions, in our

home Madison market.

I joined the bank in 1993, right before our strategic planning offsite. We had less than $100 million in

assets at the time, but we were already thinking about what else strategically fit under the business

banking umbrella. Through our active sales calling efforts, we were regularly turning away lending

opportunities that didn’t quite fit standard commercial lending, and we knew we could do more. So, in

1995, we launched our asset-based lending business, marking a pivotal point in our evolution and setting us

on a path toward becoming a diversified business bank. As we have expanded into new areas, we have

consistently hired seasoned experts to operate these businesses, both to ensure high quality service to

clients, and to avoid any unforeseen pitfalls.

What has changed most dramatically is scale and diversification.

Today, we operate across four bank markets and serve clients through a broad and integrated national

platform. Private wealth management, equipment finance, SBA lending, floorplan financing, accounts

receivable financing, bank consulting and other services now complement our traditional banking businesses.

Our diversified offerings create multiple avenues for revenue growth, including some that are economically

counter-cyclical.

Fee income diversification has also become a differentiating strength for First Business Bank over time. Over

the past 20 years, our non-interest income2 has grown at a compound average annual rate of 12% per year,

with

private wealth management service fees growing more than 14% per year. Even without the benefit of a

fee-driven residential mortgage or consumer business, our ratio of fee income to total revenue has grown to

exceed our peers in each of the past 10 years.

Of course, this change did not happen all at once. Our evolution has been deliberate, guided by successive

strategic plans and an unwavering focus on building capabilities that allow us to grow alongside our

clients.

Creating Long-Term Shareholder Value

A pivotal moment in our history was our decision to go public, which we completed in October 2005.

That step created liquidity for the original group of 167 shareholders who believed in this company when it

was little more than an idea. It also allowed a broader group of investors to participate in our growth

through our subsequent public offering.

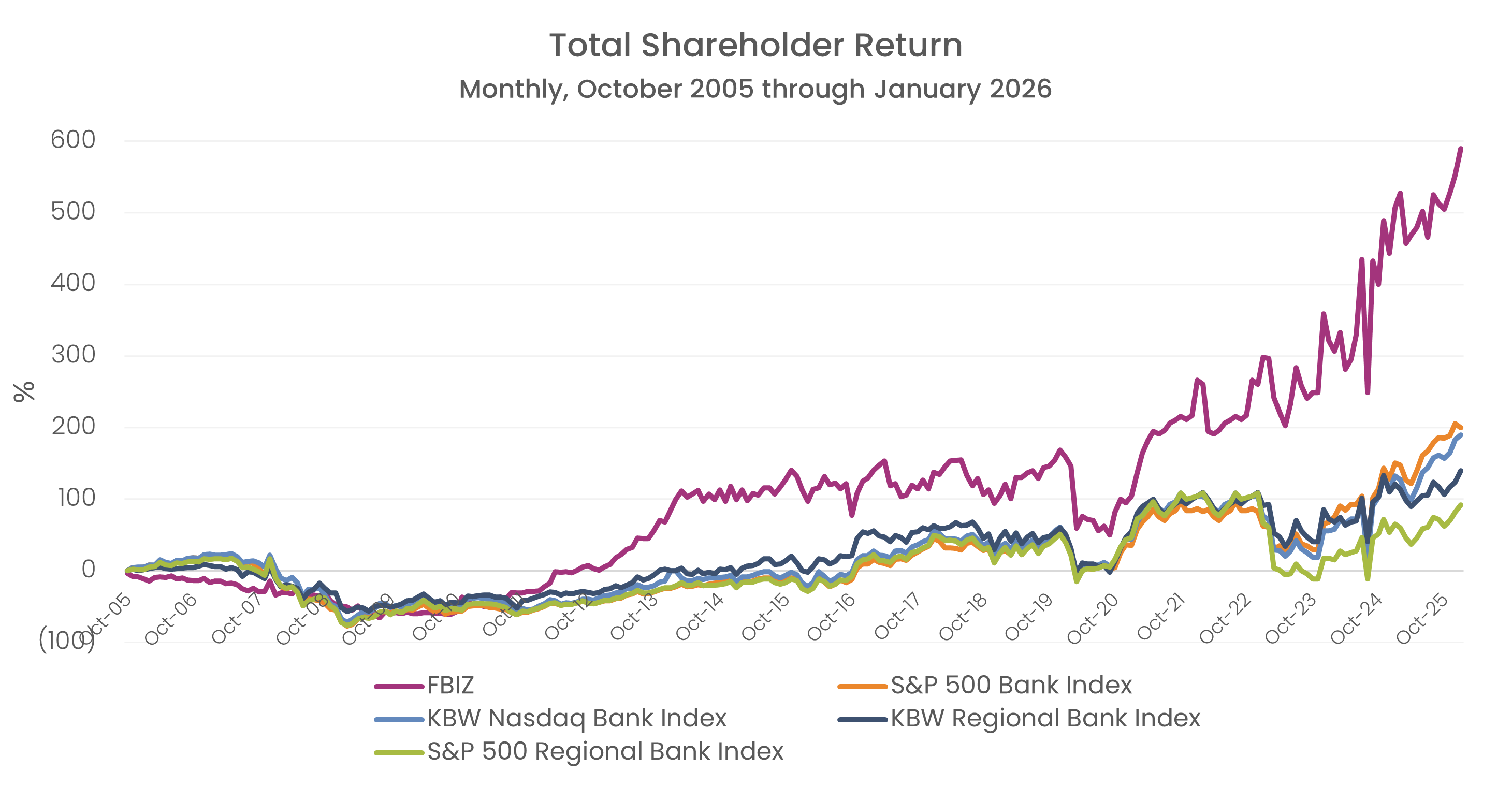

Since going public, we believe our performance speaks for itself. From October 2005 through January 2026,

FBIZ stock produced total shareholder returns of nearly 600%, exceeding the S&P 500 Bank Index by a

multiple of three and the S&P 500 Regional Bank Index by a multiple of six. It’s worth noting that

of the 7,523 commercial banks that operated in 2005, only 3,815 remain today3. Our performance has

outshined

not just a fixed index but rather a constantly shifting selection of banks that “won” in the

proverbial “survival of the fittest.”

*Source: Bloomberg

We’ve built a business model designed to generate sustainable returns over economic cycles. Our

consistent execution has supported earnings growth, dividend raises, and stock price appreciation —

building enduring value for our shareholders.

As we look ahead, our focus remains the same: disciplined growth, prudent risk management, and consistent

execution that supports long-term shareholder returns.

The Constant That Matters Most: Our People and Culture

While strategy, diversification, and performance are critical, we believe the true differentiator of our

company is culture.

Culture matters.

From the beginning, we have believed that in business banking, whoever builds the best team

wins. That belief has guided our company and continues to shape how we hire, develop, and

support our teams. By emphasizing collaboration, accountability, and long-term thinking, we create an

environment where our employees can do their best work for our clients and, ultimately, deliver sustainable

value for our shareholders.

We finished 2025 with 365 full-time equivalent employees (“FTE”) – up from 18 when I joined

bank in 1993, and up by 50% over the past decade. More importantly, we grew revenue per FTE 38%

over the past decade, contributing to our trend of 40% average outperformance on this metric compared to our

peers. Our expenses per FTE have risen at a slower pace, up 30% over the past ten years. This drove

meaningful efficiency gains, by design. A bank’s efficiency ratio measures the cost of generating

every dollar of revenue. Like a golf score, lower is better, and our efficiency ratio4 has improved by

nearly

400 basis points over the past ten years, from 62.75% for 2015 to 58.78% for 2025.

Behind our success is a deeply embedded culture of service and expertise. Client relationships drive our

business, and employee engagement drives our relationships. In 2025, First Business Bank employees again

reported high engagement. The bank earned an employee engagement rating of 85% in our externally run survey,

outperforming the industry benchmark5 of 78% and meeting our strategic plan goal. This is so important to

us

that we measure it annually as one of just seven strategic plan goals (as we did in our previous strategic

plan as well). As we grow, we know we can’t lose sight of the importance of our people and our

culture.

Exceptional employee engagement is the driver behind solid public recognition of our culture in recent years.

In 2025 we were honored to be recognized by USA Today as a “Top Workplace” in the USA

for the fourth consecutive year. We were also recognized in our local markets, including Top Workplaces

awards in Madison (awarded by WI state journal) and Southeastern Wisconsin (awarded by Milwaukee Journal

Sentinel).

When we add new talent to our staff, we tend to keep them. We are proud of the opportunities we provide for

people to grow their careers here. As the organization grows, so do the opportunities for our employees.

That continuity strengthens client relationships, preserves institutional knowledge, and creates a virtuous

cycle: success attracts great people, great people drive better results, and better results create more

opportunity.

Satisfied clients create an annuity stream, and we benchmark our performance to continuously improve and

track one particularly powerful metric: the Net Promoter Score (NPS). This is measured by an independent

firm that asks clients to rate their likelihood of recommending their bank, on a scale of -100 to +100.

First Business Bank earned an NPS score of 78 for 2025, significantly outperforming top banks in banking and

investments. This is another measure we elevated to primary importance as one of our seven strategic plan

goals.

Looking Ahead to 2026

We enter 2026 with a clear strategic plan, a diversified and resilient business model, and a team that

understands where we come from, where we are going, and how we intend to get there. While external

conditions will continue to change—as they always do—we are confident in our ability to adapt

without losing sight of the principles that have guided us for decades.

As announced last year, I will retire as CEO effective May 2, 2026, and our President and Chief Operating

Officer Dave Seiler will be named President and CEO of First Business Financial Services, Inc. Dave steered the 2024-2028 strategic plan

process and is deeply committed to our continued execution and success. I am grateful our team, our

communities, and our shareholders will continue to benefit from Dave’s deep banking experience and

dedication to excellence.

Much has changed since our founding. Many things have improved. But the most important elements—the

focus on disciplined strategy, deposit strength, long-term relationships, and a culture built around the

best people—remain unchanged.

I sincerely thank you for your relationship with First Business Bank. We are proud of what we

have built together and excited about what lies ahead.

Sincerely,

Corey Chambas, CEO

First Business Financial Services, Inc.

parent company of First Business Bank

This letter includes “forward-looking statements” related to First Business Financial Services, Inc. (the

“Company”) that can generally be identified as describing the Company’s future plans, objectives, goals

or expectations. Such forward-looking statements are subject to risks and uncertainties that could cause

actual results or outcomes to differ materially from those currently anticipated. These forward-looking

statements are made pursuant to the safe harbor provisions of the Private Securities Litigation Reform

Act of 1995. For further information about the factors that could affect the Company’s future results,

please see the Company’s most recent annual report on Form 10-K, quarterly reports on Form 10-Q, and

other filings with the Securities and Exchange Commission. We do not intend to, and specifically

disclaim any obligation to, update any forward-looking statements.